SMM May 15 Report:

Price Review:

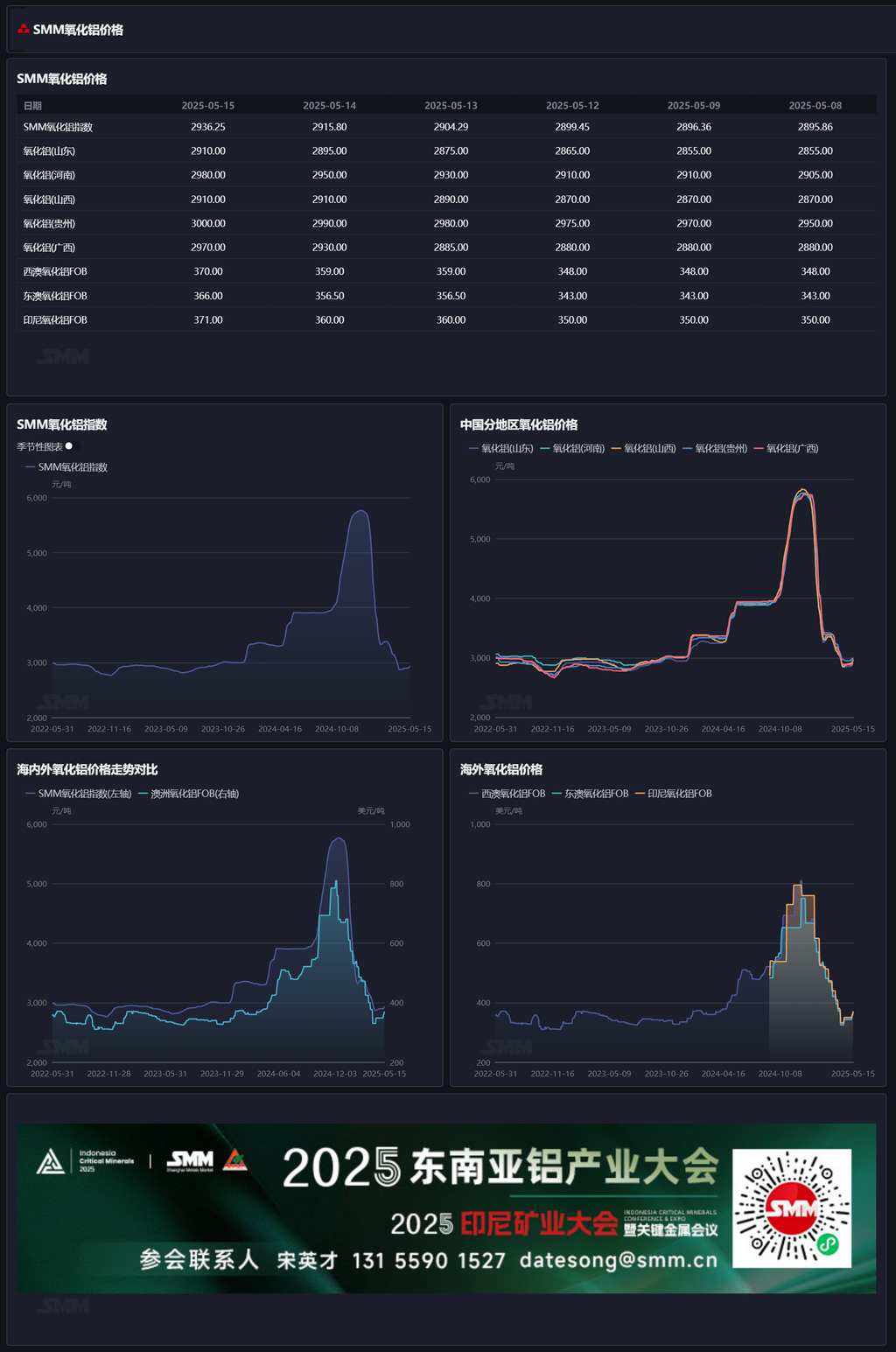

As of Thursday this week, the SMM alumina index stood at 2,936.25 yuan/mt, up 30.39 yuan/mt from last Thursday. In Shandong, prices were reported at 2,890-2,930 yuan/mt, up 55 yuan/mt from last Thursday; in Henan, prices were reported at 2,960-3,000 yuan/mt, up 75 yuan/mt from last Thursday; in Shanxi, prices were reported at 2,910-3,000 yuan/mt, up 55 yuan/mt from last Thursday; in Guangxi, prices were reported at 2,940-3,000 yuan/mt, up 90 yuan/mt from last Thursday; in Guizhou, prices were reported at 2,980-3,020 yuan/mt, up 50 yuan/mt from last Thursday; in Bayuquan, prices were reported at 3,160-3,240 yuan/mt.

Overseas Markets:

As of May 15, 2025, the FOB Western Australia alumina price was $370/mt, with an ocean freight rate of $21.50/mt. The USD/CNY exchange rate selling price hovered around 7.23, translating to an equivalent domestic mainstream port selling price of approximately 3,278 yuan/mt, which is 342 yuan/mt higher than the domestic alumina price. The alumina import window remained closed. This week, four new overseas spot alumina transactions were inquired about, with transaction prices rising from the previous period:

- On May 9, 30,000 mt of alumina was traded overseas at $358/mt FOB Western Australia, with a July shipment date.

- On May 12, 30,000 mt of alumina was traded overseas at $359/mt FOB Western Australia, or $356.5/mt FOB Eastern Australia, with a July shipment date.

- On May 14, 25,000 mt of alumina was traded overseas at $351/mt FOB Vietnam, with a late June shipment date.

- On May 14, 30,000 mt of alumina was traded overseas at $387.14/mt CIF Indonesia, sourced from Western Australia, with a late June shipment date.

Domestic Market:

According to SMM data, as of Thursday this week, the total installed capacity of metallurgical-grade alumina nationwide was 109.22 million mt/year, with a total operating capacity of 84.12 million mt/year. The national weekly alumina operating rate decreased by 2.66 percentage points WoW to 77.02%, primarily due to concentrated maintenance and production cuts in Guangxi and Guizhou. Among them, the weekly alumina operating rate in Shandong decreased by 0.92 percentage points WoW to 89.30%; in Shanxi, it remained unchanged WoW at 76.00%; in Henan, it remained unchanged WoW at 52.50%; in Guangxi, it decreased by 10.27 percentage points WoW to 84.87%.

During the period, spot alumina transaction prices rose from the previous period. By region: aluminum plants in Xinjiang conducted tender purchases for some alumina, with delivery-to-factory prices around 3,220-3,230 yuan/mt; 4,000 mt of alumina was traded in Shandong at 2,900-2,910 yuan/mt; 5,000 mt of alumina was traded in Henan at 2,980-3,100 yuan/mt; 2,000 mt of alumina was traded in Guangxi at 3,000 yuan/mt.

Overall:

This week, alumina enterprises in south China concentrated on maintenance and production cuts, with operating capacity decreasing by 2.9 million mt/year on a MoM basis, further tightening spot cargo availability. Additionally, alumina enterprises have been facing continuous losses in recent months, with a strong intention to stand firm on quotes. Coupled with maintenance and production cuts, the tightening of spot cargo availability has led to a significant rebound in spot prices. In the futures market, driven by the shift in alumina fundamentals towards a deficit, as well as news about production dynamics of domestic alumina enterprises, the revocation of mining rights of several miners in Guinea, and favourable macro front, alumina futures have rebounded strongly. In the short term, due to the concentrated maintenance and production cuts, alumina spot cargo availability is expected to remain tight, with prices expected to hold up well. However, as alumina maintenance concludes and new capacity is released, alumina operating capacity is expected to rebound. It is necessary to continuously monitor the maintenance, production cuts, and production resumptions of alumina enterprises.